What is reportable under MiFIR (MiFID II Transaction Reporting) – Analyzing Derivatives

The goal of this article is to provide a deeper look at specific investment products and analyze how they fit within Article 26 of MiFIR (legislation link). The opinions provided are based on questions from Cappitech clients about non clear-cut trading products.

Article 26 Intro

Article 26 created an obligation of T+1 Transaction Reporting that goes into effect on January 3rd 2018. The legislature focuses on investment products that are traded on a traded venue (TOTV) or a derivative based on a product that is TOTV (also called UTOTV, underlying traded on a traded venue).

ESMA defines trading venues as those registered in the EEA as Regulated Markets. Their updated list of trading venues included under MiFID II can be found here.

Text of what is reportable

Before diving deeper to analyze individual investment products and whether they are under scope for Article 26, let’s look at the text. The legislature states:

The obligation laid down in paragraph 1 shall apply to:

(a) financial instruments which are admitted to trading or traded on a trading venue or for which a request for admission to trading has been made;

(b) financial instruments where the underlying is a financial instrument traded on a trading venue; and

(c) financial instruments where the underlying is an index or a basket composed of financial instruments traded on a trading venue

The obligation shall apply to transactions in financial instruments referred to in points (a) to (c) irrespective of whether or not such transactions are carried out on the trading venue.

ISIN – an investment product’s code

To create a standard for reports, rather than using product symbols or names, MiFID II transaction reports are powered by ISIN Codes. These are 12 character alpha-numerical codes created for investment products that are listed on a trading venue. The ISIN is issued on the issuance level. Therefore, in cases such as stocks that are listed on one venue; for example the NYSE, but traded on many exchanges, they will have the same ISIN regardless of where the product is traded.

![]()

For Article 26, the report requires either the ISIN of the investment product, or as in the case for many derivatives such as CFDs, the Underlying ISIN of the derivative.

ISINs are issued and indexed by the Association of National Numbering Agencies (ANNA). ANNA provides a free lookup service of ISINs (link). In addition, ESMA operates a Reference Instrument Database of ISINs that are registered under EEA trading venues (link).

Based on the above guidelines, below are some of the frequently asked product questions received by Cappitech when analyzing MiFID II reporting eligibility

American Depositary Receipt (ADR) of EEA Stock

Despite trading on US exchanges, ADRs are reportable under MiFID II if they represent shares in an EEA stock. The ADR is represented using the ISIN of the underlying EEA stock in the ‘Underlying ISIN’ field. (Reference, see 15 Answer 11 (e) in MiFIR Q&A link)

A gray area exists with options on ADRs. According to the ESMA guidelines, a derivative is reportable to the first degree when the underlying is TOTV. Therefore, options on ADRs are a derivative of a product trading on a non-EU trading venue. In the above link, Answer 11 (a), ESMA appears to state that options on ADRs would not be reportable.

CFDs on EU TOTV products

CFDs are a derivative of another product. If the underlying is TOTV, then a reporting obligation is required. The report is filled by stating ‘XXXX’ under the Trading Venue field and filling out the underlying ISIN in the ‘Underlying Instrument Code’ field.

Included in this group of CFDs are:

- Stock CFDs of shares trading on EEA trading venues (example BP, BMW CFDs)

- Stock Index CFDs of based on Equity Index Futures trading on EEA trading venues (example DAX, CAC and FTSE CFDs)

- Fixed Income CFDs based on Government Bond futures trading on EEA trading venues (example GILT and BOBL futures)

CFDs on EU TOTV products – No ISIN

In some cases, a CFD may be based on an EU TOTV product that there is no ISIN issued. Further review is required to understand whether the product is reportable.

The lack of an ISIN may be the result of the trading venue not yet having registered the product. In this case, the trade should be reportable when an ISIN is made available.

In addition, a trading venue may not have the obligation to register an ISIN. As mentioned above, ISINs are registered on the product issuance level. Therefore, a trading venue may not have to register an ISIN if one exists.

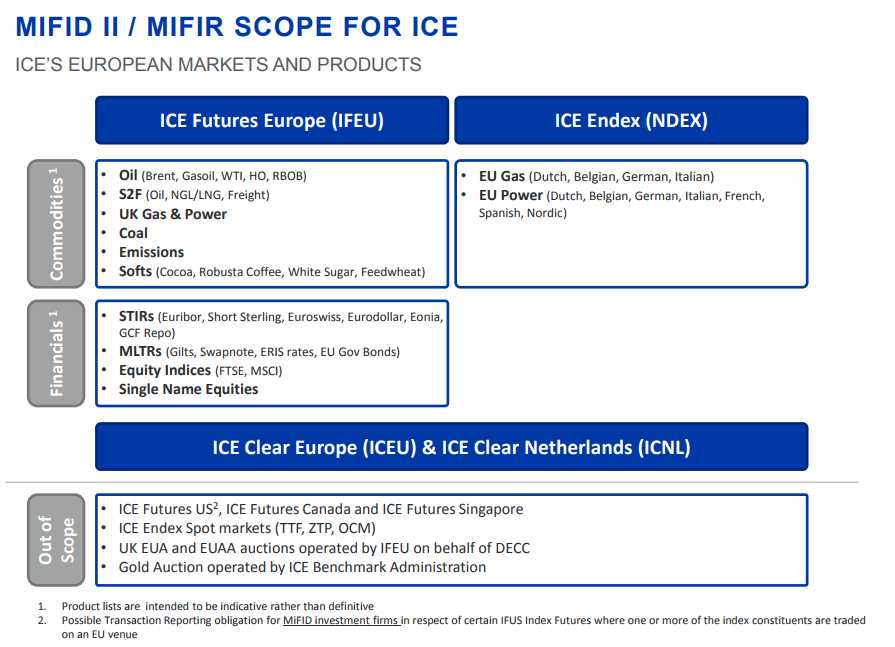

CFDs on Oil

The most popular oil CFDs are Brent Crude (BRN) and West Texas Crude (WTI). The products are based on underlying futures from the ICE and CME (NYMEX) exchanges. In terms of Article 26 scope, CFD providers need to verify which is the underlying future for their products.

ICE crude oil futures are TOTV and reportable as they are listed on ICE Europe.

CME crude oil futures aren’t TOTV and not reportable as they are US traded.

In a presentation for members, the ICE defined in June 2017 their interpretations of products being in and out of scope. According to the ICE, in advance of MiFID II, the exchange plans to issue ISINs for futures products falling under scope ahead (as of late December, some product ISINs such as for BRN haven’t yet been published by ANNA)

CFDs on US shares (dual listed)

Another gray area are CFDs on US stocks that are dual listed. For example, shares of AAPL and GE are traded in both the US and EEA trading venues. Unlike ADRs where a new product is issued for the US market, AAPL and GE trades in Europe are the same shares that exist in the US and use the same ISIN.

The result is that CFDs on AAPL shares have an ISIN that does trade on EEA based trading venues. This would seem to confirm that CFDs on dual listed US shares are reportable.

On the other hand, one can argue that the immediate underlying product of which the CFD price is based on is US traded. Under this assumption, the CFD won’t be reportable.

On the other hand, one can argue that the immediate underlying product of which the CFD price is based on is US traded. Under this assumption, the CFD won’t be reportable.

ESMA doesn’t directly provide an answer about CFDs for dual listed products. However, in their RTS, under the definition of ‘Underlying Instrument Code’ it states:

For derivatives or other instruments which have an underlying, the underlying instrument ISIN code, when the underlying is admitted to trading, or traded on a trading venue.

The ESMA language would appear to include CFDs of any product that the underlying ISIN has representation within an EU trading venue.

Spot Precious Metals and CFDs

For the most part, precious metals based on spot prices such as Gold (XAU/USD) and Silver (XAG/USD) are traded Over the Counter (OTC).

The OTC designation for spot Gold and Silver is an important for MiFID II purposes when it comes to Gold and Silver CFDs. As these CFDs are based on products that are OTC and not TOTV, they are not under scope of MiFIR transaction reporting.

ESMA provided a clear explanation for this in their TOTV Opinion that they issued in May 2017 (link). In their opinion, they exclude CFDs based on products that are OTC themselves and don’t have reference data details from a trading venue.

Spot FX and CFDs

Like precious metals, forex is also a spot based investment product based on OTC trading. The result is that OTC derivatives such as spreadbets, CFDs and margin forex that are based on spot FX prices aren’t UTOTV. Therefore they don’t fall under scope.

ESMA provided a clear explanation for this in their TOTV Opinion that they issued in May 2017 (link). In their opinion, they exclude CFDs based on products that are OTC themselves and don’t have reference data details from a trading venue.

MTFs, OTFs and Systematic Internalizers (SI)

Among the changes of MiFID II is a broadening of the definition of Trading Venues. Beyond regulated exchanges, also deemed trading venues are products traded by Systematic Internalizers (SI), Multilateral Trading Facilities (MTF) and Organized Trading Facilities (OTF). Products listed on these venues may require the venue to issue an ISIN and trades on them are under scope for MiFIR Transaction Reporting.

An example of an MTF is LMAX. Traded on LMAX are CFDs for equity index and commodities as well as FX products. As such, although the LMAX CFDs are similar to OTC based CFDs, they fall under scope due to their TOTV status.

Worth noting is that many CFDs on LMAX have contract specifications that are slightly different than similar CFDs marketed by OTC brokers.

CFDs on Cryptocurrencies

Becoming very popular in 2017 are CFDs on cryptocurrencies. This includes CFDs for Bitcoin, Ehtereum and Litecoin. The products first raised a question for EMIR Reporting and whether they are under scope.

Becoming very popular in 2017 are CFDs on cryptocurrencies. This includes CFDs for Bitcoin, Ehtereum and Litecoin. The products first raised a question for EMIR Reporting and whether they are under scope.

For MiFID II reporting, the answer of under scope is much simpler than EMIR as cryptocurrencies are fully OTC and not under scope. Although cryptocurrencies are traded on exchanges, none of them registered trading venues under ESMA.

However, this may change in the future. The CME Group in the US launched Bitcoin Futures this month. As such, this could trigger momentum to EU based trading venues to launch similar products. In addition, existing non-regulated cryptocurrency exchanges may receive regulated statuses in the future.